Dr Alex Davies unexpected path to practice ownership

She never thought she’d want to own her own practice but then circumstances changed, and Dr Alex Davies had a change of heart.

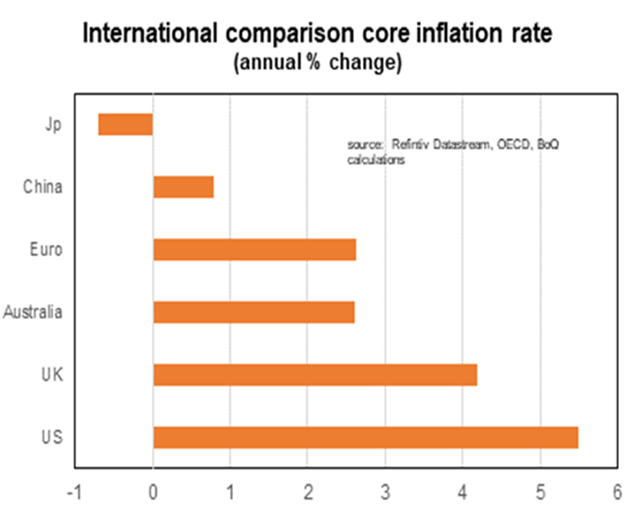

Learn MoreFor much of the past decade the main economic problem facing Australia was that economic growth had not been strong enough for long enough. Increasingly the new problem looks like it will be inflation. The Q4 CPI numbers was the third consecutive quarter that the annual growth of inflation was above the RBA’s target band. The annual growth rate of one of the measures (‘trimmed mean’) was at 2.6%, its highest level since 2014.

The big picture is that demand has been a lot stronger than supply leading to pricing pressure. This has been mainly for goods although the prices of many services are not unusually low. The hope has been that global supply constraints would prove to be temporary and diminish as factories ramped up production and the logistics of transport and storing of goods improved. But then the Omicron wave appeared. Signs that the Omicron wave is starting to subside in Australia and other areas of the world gives hope that some of the recent supply problems will improve in coming weeks. But we don’t know for sure when. Even if everything does go smoothly on the virus front supply problems will last at least into the second half of this year.

It is also possible that there will be permanent changes to the economics of the supply of goods and services. Global supply chains had been set to maximise efficiency and minimise costs. Following their experiences of COVID and rising geo-political tensions a growing number of firms have indicated their desire to diversify their sources of supply and hold more inventories.

Another longer lasting supply concern might be the lack of skilled workers. A return of strong immigration flows is likely to be the best solution in the short term to meeting the strong demand for workers (improving education and training is a good solution in the long term). The opening up of borders will help. But the reappearance of Omicron and understandable ongoing caution of governments and people means it is likely to be sometime before immigration returns to pre-COVID the levels.

But as has become increasingly clear rising inflation pressures is also about strong demand. Demand for goods should moderate as consumers rebalance back towards services as spending patterns gradually return to ‘normal’. But the economic rebound has been a lot stronger than virtually everyone has forecast.

Monetary policy is currently set at emergency levels at a time when the economy is either at or close to full employment. Inflation is above the top end of the target band. Wages growth is currently under target but all the signs are that it will pick up. Fiscal policy remains extremely supportive. One measure of the stance of monetary policy (real cash rate, or the cash rate after inflation) is at its most economically supportive level in over 40 years. In a world of increasing interest rates if Australia does nothing in effect they are easing monetary policy.

In this light it is virtually certain that the RBA will end Quantitative Easing in February. I have pulled forward my expectations of when the RBA will first move the cash rate into the fourth quarter, when I expect a 15bp rise (to 0.25%) in November followed by another quarter percentage point expect rise in December (to 0.5%). It is possible that the RBA could move even earlier. Financial markets have priced the first move (0.15%) now essentially by May. Whether the RBA does move that early will depend upon how the wages numbers print in late February.

We have a range of offers tailored specifically to your profession. Plus, our strong relationship with industry partners means you can access special discounts and promotions from our preferred suppliers.