Dr Kate Lindsay's against the odds

Her new business had only just opened when COVID-19 struck, yet Dr Kate Lindsay says she’s not too worried.

Learn MoreIn the couple of weeks before Omicron parts of Europe and the US were fighting rising virus numbers of the Delta strain. Australia should be in a better state than Europe and the US is currently by winter-time (when the spread of the virus is more likely). We have a higher vaccination rate, and most of the population are likely to recently have had a booster shot by then. The arrival of a new variant has added caution. But there is a good chance that an updated vaccine could be in play by mid next year. The ongoing issue is how Governments’, consumers’ and firms react to the news of the emergence of a new virus strains or rising case numbers. In time society will get more comfortable that the health system will be able to minimise (but not eliminate) the risk of COVID.

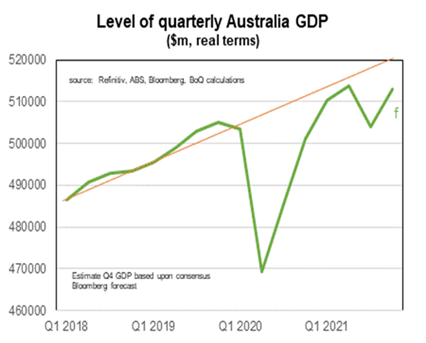

The Q3 GDP growth of -1.9% was worse than any single quarterly decline during the 1990s recession. But it was half as bad as the -4% that some forecasters were expecting a few weeks back. The main driver of the big drop was the Sydney, Melbourne and Canberra lockdowns. With those lockdowns now at an end a substantial bounce in economic growth is likely in the December quarter.

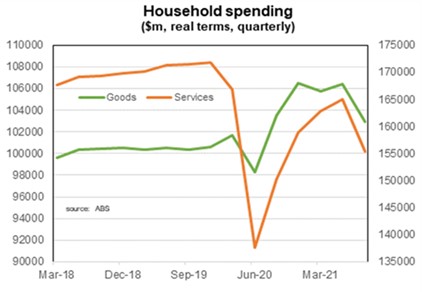

Typically declines in GDP would be a cause of major angst. It has not been on this occasion as the Government has been very successful in buffering household and incomes from the fallout of the pandemic. The impact of COVID can be more clearly seen on quarterly household spending that was over 3% below December 2019 levels at the end of September 2021.

COVID has impacted not only how much consumers spend but also where they have been spending it. Spending on goods is comfortably above its pre-COVID trend. COVID though has severely impacted spending on services. Extremely low interest rates, the rapid rebound in the economy and government support programs has seen investment of all types rise following the nationwide lockdown in 2020.

COVID has had a differential impact between industries and between states. Demand in the regions that have endured lockdowns (Victoria, NSW and the ACT) was particularly weak in the September quarter. There has continued be growth of economic activity in the other states.

The Government was able to provide massive fiscal support because for some time Australia ran a very conservative fiscal policy (modest deficits, low debt). An argument could (and was) made that pre-COVID fiscal policy should have been more supportive of the economy. The low level of debt meant that the Government was able to comfortably provide substantial support to the economy very quickly. That should be taken into account when setting fiscal policy in the future.

The maintenance of strong income growth has allowed for strong spending on the stuff that households and firms could buy (such as cars, equipment) and rising saving (because they couldn’t buy services). This created a demand-supply mismatch as lockdowns and other restrictions meant that production of goods was unable to keep up with demand. This will change as factories everywhere again get back to full capacity (that already is happening) and more spending switches back to services and away from goods. A lot of attention on the demand-supply mismatch has been on the supply problems. But with a high level of saving and very tight labour markets it is likely that demand will remain strong. Both the Federal Government and the RBA have begun dialling back fiscal and monetary support to the economy.

We have a range of offers tailored specifically to your profession. Plus, our strong relationship with industry partners means you can access special discounts and promotions from our preferred suppliers.