Rebuilding a medical practice

Rebuilding a practice and career in a new country is challenging enough, but Dr Bobby Chhoker had an even grander plan.

Learn MoreAs expected the RBA increased the cash rate by 0.5 percentage points following the July meeting (the cash rate is now 1.35%). The cash rate increased for the reasons you would expect. Inflation is well above the 2-3% target and the labour market is very strong.

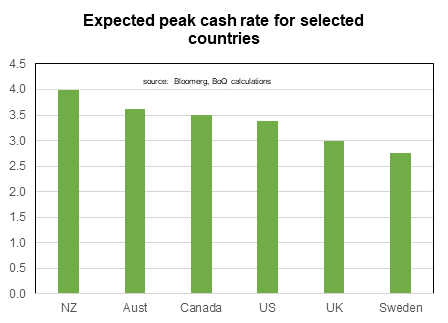

Unless something unexpected happens the RBA made it clear that there are more rate hikes to come. The RBA will want to get to at least a 2% cash rate relatively quickly. That suggests another big move (most probably 0.5 percentage points, but a 0.4 percentage point move is a possibility) at the August meeting. Given that the Q2 CPI (released 26 July) is likely to show another big quarterly rise such a big move will be easy to justify.

Thereafter I think the RBA will start to slow the pace of interest rate rises in order to get a better idea of what impact the rate hikes to date have had. A 0.25 percentage point move at either the September or October meeting would take the cash rate to 2% (or a bit over). A final 0.25 percentage point move (taking the cash rate to 2.25-2.35%) for the year is then likely at the November meeting following what is likely to be another large Q3 CPI number (released 26 October). At the time of writing, financial market pricing is for the cash rate to be 3% by end 2022. The median economist forecast is 2.35%.

On the announcement government bond yields declined and the $A fell, I thought the RBA’s statement was relatively balanced (emphasising the need to fight inflation but also the downside economic risks). Other central banks have been more aggressive in talking about higher interest rates in recent times.

The RBA thinks that inflation will hit 7% this year before declining back towards the 2-3% band next year. Maybe that will be the case although inflation has been higher than expected and supply problems have lasted longer than anticipated. This suggests that the risks for the RBA’s inflation forecasts are probably still to the upside.

The rate hikes that have already occurred is impacting sentiment about house prices although growth had begun to decline at the start of this year reflecting concerns about affordability. The first monthly decline in major city house prices took place in May (the first rate hike) although that was mainly in Sydney and Melbourne.

That house prices will decline as interest rates rise would not surprise the RBA (although they might be surprised how quick that decline has started). In their April Financial Stability Review the RBA noted that historically a 2 percentage point increase in interest rates has typically led to a 15% decline in real house prices (i.e. house price growth after allowing for inflation) over a two-year period. The interest rate rise in this cycle will almost certainly be more than 2%. But inflation could be up 10% over 2022 and 2023. This means it is possible that real house prices might decline by 20-25% by end 2023 but actual house prices fall by ‘only’ 10-15%.

Falling house prices impact the economy in various ways. People are less likely to build or buy a house when their value is falling. Small businesses borrow against the value of their home, so a declining price reduces how much they can borrow. Consistent reminders that the value of your house is going down can’t be a good thing for consumer confidence.

More directly there has been plenty of research indicating that falling house prices (and therefore a drop in household wealth) leads to lower consumer spending (and the wider economy). How big a negative is less certain, as it depends upon the state of the economy and what is happening with monetary and fiscal policy.

Currently the economy is in good shape, with the unemployment rate around fifty-year lows. Household have socked away a mountain of saving over the past couple of years although they are currently being hit with a significant inflation tax. The type of spending typically impacted by changes in wealth (the RBA found that spending on cars, furnishings and clothing are the most strongly impacted by wealth changes) is the spending that has been strongest during COVID and would be expected to slow anyway.

Most surveys indicate that consumer sentiment is currently extremely negative. Higher interest rates have played a role but higher inflation is the biggest issue. The May retail sales data highlights that consumer spending so far has remained strong. But declining house prices, rising interest rates and negative real wages growth means the risks are that consumer spending may be slower than anticipated sooner. And is the reason why the RBA is keeping a careful eye on developments on what households are doing with their money.

We have a range of offers tailored specifically to your profession. Plus, our strong relationship with industry partners means you can access special discounts and promotions from our preferred suppliers.